[ad_1]

This piece beforehand appeared within the CLS Blue Sky Weblog.

Within the international effort to guard the earth’s local weather, the tempo of regulation is rivaled solely by the velocity of technological innovation.

What appeared unbelievable just some years in the past – requiring giant firms to measure and report annual greenhouse gasoline emissions generated by their operations and “worth chains”– is changing into actuality in a number of international locations.

Whereas the SEC’s local weather disclosure guidelines are pending, and can most likely face litigation when remaining, rules from different companies and jurisdictions are more likely to have an effect on U.S. firms quickly:

The European Union’s “Company Sustainability Reporting Directive” (CSRD), which fits into impact in January,

the Federal Acquisition Regulatory (FAR) Council’s November 2022 proposal on “Disclosure of Greenhouse Gasoline Emissions and Local weather-Associated Monetary Threat”,

California’s new “Local weather Company Information Accountability Act” (SB 253) and “Local weather-Associated Monetary Threat” statute (SB 261), in addition to its “Voluntary Carbon Markets Disclosures” invoice (AB 1305), all signed into legislation in October, and

New York State’s twin payments for a “Local weather Company Accountability Act” (S897-A) and a “Local weather-related monetary threat and required disclosures” statute (S5437), which can be authorized within the coming months.

All these rules would require firms to make disclosures much like these on the coronary heart of the SEC’s March 2022 proposal “on The Enhancement and Standardization of Local weather Threat Disclosure:”

the dangers and better prices firms count on to face on account of local weather change (so referred to as “climate-related monetary dangers”), and

their greenhouse gasoline emissions knowledge (together with Scope 1, Scope 2, and Scope 3[1]).

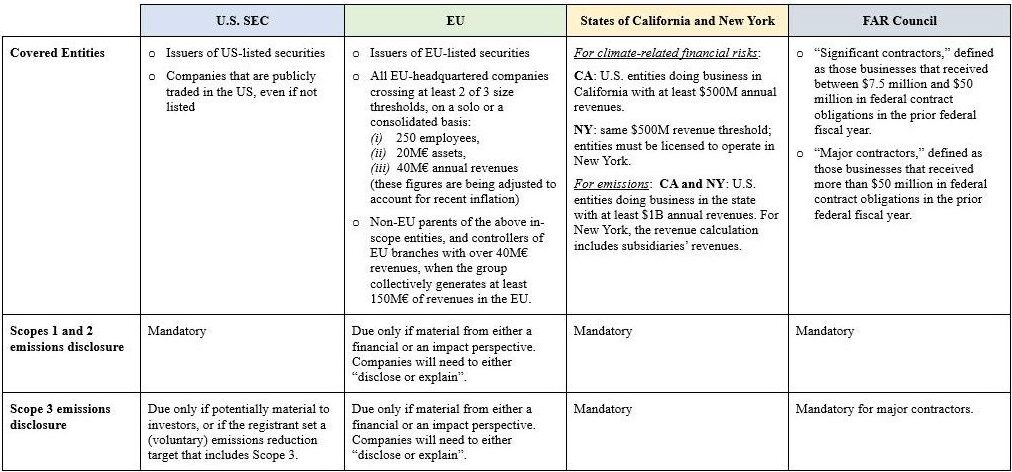

A Simplified Comparability

Key Variations

Consolidation – Each the EU and U.S. regulators think about an organization’s dimension in figuring out which entities are topic to the measures, how quickly these measures apply, and what data these firms are required to reveal (with extra disclosure anticipated from bigger entities).

EU – The CSRD units remarkably low thresholds general. Additional, these thresholds apply on a consolidated foundation, which means that the revenues, property, and worker totals should be added up throughout a whole group. As well as, non-EU teams might want to report on the degree of their final holding firm

California – California has set a a lot larger size-threshold than the EU ($1 billion for emissions reporting, and $500,000 for climate-related dangers) however doesn’t point out the way it ought to be calculated. Implementing guidelines should nonetheless be issued by the California State Air Sources Board (CARB) within the coming 12 months and should direct using consolidated-group figures. If CARB doesn’t so point out, the variety of lined firms might be considerably smaller.

New York State – New York follows California’s income thresholds, nevertheless subsidiaries’ revenues are explicitly included within the depend.

SEC – Not like the opposite three measures, the SEC’s proposed guidelines would apply solely to publicly-traded firms. The foundations might be phased in progressively based mostly on an issuer’s dimension, decided by the worth of its public float.

Group-level disclosures – With one exception, these measures additionally require reporting to be finished on a consolidated foundation.

SEC – Underneath the SEC’s proposed guidelines, securities issuers would report on local weather within the mixture, on behalf of themselves and their managed subsidiaries, simply as they do for his or her financials.

California and New York – The identical precept will seemingly apply in California and New York. As soon as an organization is roofed (by advantage of no matter consolidation methodology), it might want to disclose mixture local weather dangers and emissions for itself and its subsidiaries.

EU – The EU will apply the identical precept on a primary degree. Nevertheless, the CSRD features a separate provision (Article 40a) that can require teams to report additionally on the degree of their final holding firm, no matter the place that holding firm could also be headquartered or listed, so long as the group generates a big mixture income on EU soil. This provision casts an awfully broad web – though it will likely be a minimum of 6 months (till the implementing requirements for Article 40a are launched) earlier than the necessities are clear on what final dad or mum stories should embody for non-EU teams (and notably whether or not they should embody group-wide emissions).

Materiality qualifier (from most to least stringent):

California and New York State – California and New York (if handed) would require necessary disclosure of Scope 1, 2, and three emissions.

FAR Council guidelines – The FAR would additionally require public emissions knowledge, though Scope 3 solely from main contractors.

SEC – Scope 1 and a couple of emissions disclosure can be necessary for all SEC registrants. Scope 3 can be required provided that the emissions are “materials”. The materiality qualifier is according to the SEC’s definition of monetary materiality and the related U.S. Supreme Courtroom precedents and so ought to be tied to the “substantial chance” {that a} cheap investor would think about the info necessary when investing or voting choice. The SEC notes that disclosure of Scope 3 emissions could also be mandatory to present an entire image of a registrant’s climate-related dangers.

EU – The CSRD would require disclosure of Scope 1, 2, and three emissions solely to the extent that an organization deems every related from a double materiality perspective – which means from each a monetary and a climate-impact perspective. The climate-impact disclosure will seemingly be broader. When assessing affect materiality, firms are anticipated to think about the wants of all their “stakeholders” – which embody “civil society, NGOs, governments, analysts and teachers”.

You will need to be aware that the completely different materiality assessments of those disclosure regimes may yield various outcomes.

Some firms (for instance, these in heavy trade, relying on their specific buyer pool) could solely deem Scope 1 and a couple of emissions materials to their actions, whereas for others (corresponding to transportation firms) materials emissions will all be beneath Scope 3. The failure to reveal a number of classes will after all hinder comparisons between firms and should lead to an incomplete image of a agency’s emissions and transition threat.

Carbon accounting methodologies:

EU – The EU Directive permits firms to use GHG Protocol accounting methodologies on a par with the Worldwide Standardisation Group’s (ISO) 14064 steering on GHG, and the EU Fee’s Suggestion (EU) 2021/2279 on environmental footprint strategies. Though these frameworks are comparable, their wording and diploma of specificity range (with the GHG Protocol being extra detailed and prescriptive than the remainder), opening probably to a various interpretation of what are in observe minutely exact accounting and consolidation methods.

California – The California statute references the GHG Protocol – with an added, considerably ambiguous reference to “an alternate normal, if one is adopted after 2033”.

New York State – The New York invoice references the GHG Protocol, requirements developed by CDP World, and any guidelines which may be adopted by the SEC.

FAR Council – FAR equally references the GHG Protocol, CDP, and different main worldwide carbon accounting frameworks

SEC – Whereas the proposal was based mostly on the GHG Protocol, the SEC didn’t undertake all its options and left firms free to design the carbon accounting methodology that’s greatest suited to their actions, so long as they disclose the underlying ideas and assumptions.

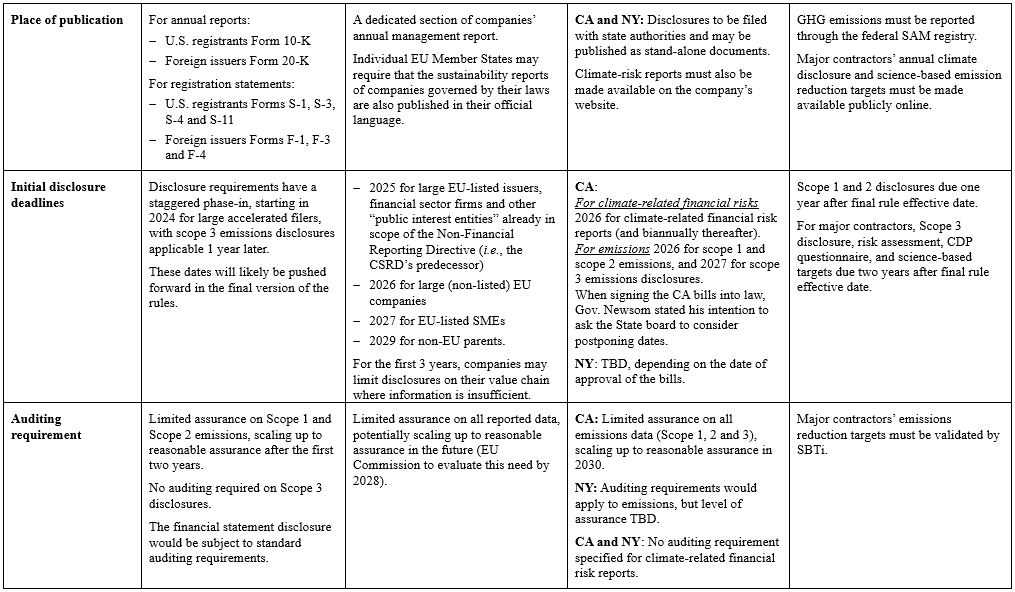

Auditing – Given the variations on this entrance, it’s seemingly that the bar on emissions knowledge assurance can be set by the framework with the very best verification requirements, which is at the moment California, requiring cheap assurance on Scope 1 by means of 3 from 2030 onwards.

Sanctions – That is the place regimes are almost certainly to range. Importantly, the sensitivity and novelty of those frameworks enhance the chance of discrepancies in enforcement type and administrative penalties throughout jurisdictions.

The Pull Results of Vanguard Regimes

Given the fragmented, quickly evolving insurance policies, multinational companies topic to a number of emission-disclosure regimes could need to adjust to separate frameworks directly.

Hypothetically, a conglomerate could need to calculate emissions and report them as soon as on the degree of its EU entities or EU sub-group (and individually, within the case of distinct EU sub-groups), one other time all the time within the EU, on the degree of its non-EU final dad or mum firm (the place completely different, or the place a special consolidation perimeter applies), and (probably, a number of) different instances on the degree of its U.S. entities (maybe on consolidated group actions, maybe not, maybe each), every time beneath completely different nationwide or state reporting guidelines.

Take Sony. The group would seemingly be caught (i) as soon as by EU CSRD guidelines, on the degree of Sony Europe B.V. (disclosing for itself and its subsidiaries), (ii) as soon as extra by CSRD guidelines (though this time beneath presumably simplified Article 40a reporting requirements), on the degree of its Japanese dad or mum, Sony Group Company (disclosing on the behalf of your complete group), and (iii) probably a number of extra instances for any entities which are both (a) registered as securities issuers with the SEC (in keeping with accessible EDGAR knowledge, these are Sony Group Company, Sony Corp. of America, Sony Monetary Holdings Inc., and Sony Music Leisure Inc.), (b) energetic in California or New York, or (c) U.S. federal authorities contractors.

Some frameworks make allowances for this anticipated overlap. The California legal guidelines will permit lined entities to submit stories generated to adjust to considerably comparable federal guidelines (such because the FAR Council or the SEC local weather disclosure guidelines, if they’re handed). The EU Fee is liable for creating a global equivalence framework that will permit firms to submit local weather stories ready beneath competing frameworks just like the SEC guidelines – though these would seemingly should be supplemented to cowl the numerous different ESG-related disclosure necessities which are constructed into the EU Directive.

Greatest practices for local weather disclosure will seemingly converge. We reference Brussels’s and California’s well-known “pull” impact, which drives a common shift of company behaviour towards jurisdictions with probably the most stringent regulatory requirements. These results could possibly be notably robust right here, given the numerous overlap among the many firms lined by every framework.

Information substantiates a big potential overlap. Over 6,000 firms are registered with the SEC (most of them U.S.-headquartered). The EU Fee had initially estimated that 4,000 international securities issuers can be lined by the CSRD. Article 40a introduced the estimated variety of international in-scope firms to 10,000 – about one-third of them U.S.-headquartered. The California statute ought to cowl 5,000 U.S. firms for emissions disclosures ($1 billion threshold), and 10,000 U.S. firms for climate-risk stories ($500,000 threshold). An October report by Public Citizen estimated that 75 % of Fortune 1000 listed firms fall throughout the scope of the California guidelines. Comparable issues apply to New York. The FAR Council anticipates that over 5,700 vital and main contractors might be affected by its proposed guidelines. Most firms caught by these different-sized swimming pools will seemingly be the identical entities.

An Alternative for SEC Management

The SEC’s rulemaking authority rests on the powers granted to it beneath sections 7, 10, 19(a), and 28 of the Securities Act, and sections 3(b), 12, 13, 15, 23(a), and 36 of the Trade Act. These federal rules permit the SEC to require that U.S. securities issuers make all disclosures which are “mandatory or applicable within the public curiosity or for the safety of buyers.”

The fee first discovered that environmental disclosure may promote investor safety in 1973. Given at this time’s heightened local weather emergency, and the markets’ clear notion of local weather threat as a supply of monetary vulnerability and volatility, this mandate ought to be obvious from a easy studying of the fee’s statutory authority.

There’s a compelling case for the SEC to take accountability for harmonizing local weather disclosure regimes within the curiosity of investor safety. As Prof. Joseph Grundfest noticed in his latest feedback to the SEC proposal, the SEC’s rulemaking may function a standardized “clearing home” for the varied local weather disclosures issued by registrants, whether or not voluntarily or necessary. Effectively over 30 international locations have adopted or will quickly undertake local weather disclosure guidelines. Mandating disclosure within the presence of personal ordering is a typical incidence, according to the SEC’s historic strategy to creating disclosure guidelines. Certainly, that is what the fee did with respect to worldwide monetary reporting instantly after its inception, beginning within the Thirties and resulting in GAAP.

Any guidelines the SEC proposes should facilitate effectivity, competitors, and capital formation – which is why the SEC should additionally conduct a cost-benefit evaluation. Compliance with the SEC local weather disclosure guidelines shouldn’t, for many registrants, require vital extra prices, as a big proportion of U.S. registrants, and most teams with international operations, will quickly be publicly disclosing extra emissions knowledge than the SEC proposes to require, even when the fee’s guidelines by no means take impact. That is with out contemplating that, within the 20 months because the SEC proposal was launched (and the SEC’s first cost-benefit evaluation carried out), the proportion of firms which are voluntarily disclosing their emissions and local weather dangers has risen considerably. In parallel, the price of buying local weather and emissions knowledge has declined and can proceed to say no. The SEC is poised to guide globally in defending buyers from climate-related monetary threat and making certain a harmonized strategy to local weather disclosures – that are solely destined to develop into extra related and widespread.

Past Investor Safety

It’s tough to say whether or not management on local weather will come from the SEC. The truth that FAR will seemingly find yourself being the extra incisive – and extra sturdy – disclosure regime on the U.S. federal degree begs consideration. Past investor safety, the variation and mitigation of local weather change is an pressing matter of environmental and industrial coverage. Residents and future generations are in want of brave and incisive local weather coverage, no matter whether or not and the way they might be impacted by monetary funding methods and returns. The CSRD is a software constructed with that ambition. The U.S. ought to take inventory.

ENDNOTE

[1] The GHG Protocol categorizes company greenhouse emissions into three broad scopes, that are probably the most extensively used reference framework for carbon emissions accounting:

Scope 1 = All direct GHG emissions originated by an organization’s personal actions;

Scope 2 = Oblique GHG emissions from consumption of bought electrical energy, warmth or steam; and

Scope 3 = Different oblique emissions that happen within the reporting firm’s broader “worth chain”, each upstream and downstream. The worth chain can embody actions associated to the extraction and manufacturing of bought supplies and fuels (and so probably direct and oblique suppliers), transport-related actions in automobiles not owned or managed by the reporting entity, electrical energy not lined in Scope 2, different outsourced actions, and even the emissions tied to using merchandise offered (estimated over the lifetime of the product) and waste disposal actions.

[ad_2]

Source link